What SACCOs are and why they matter

At their core, SACCOs are member-owned cooperatives where individuals contribute savings into a shared pool. These pooled funds are then used to provide loans to the same members. The model is simple but powerful: collective savings create collective opportunity.

Unlike informal savings groups such as rotating “merry go rounds”, SACCOs in Uganda operate within a formal regulatory framework. They are registered, licensed, and supervised, making them a safer alternative for people seeking structured financial services without the complexity of commercial banking.

SACCOs resemble banks in that they offer savings and loan facilities. However, their purpose and design differ significantly. SACCOs are built around specific groups with shared goals such as farmers, teachers, youth, women, or local communities, such that profits are shared among members rather than external shareholders. Their loan interest rates are often lower, and their savings culture is intentionally communal.

Banks, by contrast, provide a much wider range of financial products: international trade services, forex, investment banking, digital payments, and tailored personal or business solutions. For individuals or groups with more complex financial needs, banks remain indispensable. But for many Ugandans, SACCOs offer an accessible starting point for building financial discipline, accessing affordable credit, and earning returns on savings.

The trust factor behind SACCOs: Benefits and risks explained

SACCOs in Uganda draw much of their strength from trust. They are built on social proximity; people who live, work, farm, or trade together pooling their resources so everyone has a fair chance at saving and borrowing. This closeness reduces the intimidation often associated with formal banking and replaces it with a sense of shared responsibility. Members know one another, understand each other’s financial realities, and feel more confident contributing to a system rooted in community rather than distant institutions.

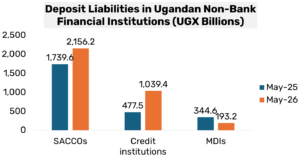

This trust driven model is reflected in national data. The FinScope Uganda 2023 Survey shows that SACCOs recorded the largest increase in usage of any formal financial service, rising from 5 percent to 14 percent between 2018 and 2023. By May 2026, member contributions reached UGX 2,156 billion, far exceeding customer deposits in credit institutions (UGX 1,039.4 billion) and microfinance deposit‑takers (UGX 193.2 billion). Such growth signals a broader shift: Ugandans are gravitating toward financial institutions that feel relatable, accessible, and community rooted.

A major reason for this rise is the way SACCOs lower barriers to financial access. Unlike banks, which typically require land titles, vehicle logbooks, or other formal collateral, SACCOs allow members to borrow based on their savings history, participation, and reputation within the cooperative. This collateral free lending model is transformative in a country where many people do not possess formal assets. Farmers without land titles, traders without registered businesses, and informal workers without documentation can access credit that would otherwise be out of reach.

Beyond credit access, SACCOs help members build disciplined savings habits through regular contributions. They return profits to members rather than external shareholders, reinforcing a sense of ownership and shared benefit. For many households and micro entrepreneurs, SACCOs have become a practical bridge into the formal financial system.

Yet SACCOs are not without risks. The same social closeness that builds trust can also obscure governance weaknesses. Leadership is often drawn from within the community, and while this fosters familiarity, it can also lead to poor record keeping, limited financial expertise, or reluctance to challenge mismanagement. Some SACCOs operate without proper licensing, leaving members exposed because they lack mandatory reserves and regulatory oversight. Liquidity pressures can emerge when many members withdraw savings at once or when borrowers default during economic shocks. And because SACCOs typically serve narrow groups such as farmers, teachers, or traders, any shock affecting that group can ripple through the entire cooperative.

The rapid rise in SACCO usage therefore reflects both opportunity and vulnerability. Their growth demonstrates how deeply Ugandans value financial institutions that feel human and accessible. But it also underscores the importance of strong governance, transparent leadership, and regulatory compliance.

Regulation: How Uganda protects SACCO members

SACCO regulation has recently undergone important institutional changes. The Microfinance Regulation Department, now under the Ministry of Finance, Planning & Economic Development, licenses and supervises SACCOs. This department replaced the Uganda Microfinance Regulatory Authority (UMRA), which was dissolved in November 2024 due to government rationalisation. Despite the administrative shift, regulatory requirements remain intact.

SACCOs with savings below UGX 1.5 billion continue to be licensed and supervised under the Tier 4 Microfinance Institutions and Money Lenders Act, 2016. Once a SACCO reaches UGX 1.5 billion in savings and UGX 500 million in minimum capital, it is classified as a large SACCO. At this point, licensing shifts from the Microfinance Regulation Department to the Bank of Uganda. This transition reflects increased risk because larger deposit pools require stronger oversight.

This regulatory tiering ensures adequate emergency reserves, sustainable lending practices, sound investment decisions, and protection of member savings. One of the most important regulatory requirements for SACCOs is the mandatory reserve fund. Every licensed SACCO must set aside at least 10% of its annual profits to build reserves. These reserves act as a financial buffer, reducing the risk of collapse and enforcing discipline in how member deposits are managed. For members, this rule is more than a technical requirement that ensures that their savings are protected.

SACCO governance: What members should look for

Good governance is the backbone of a healthy SACCO. When leadership is strong and transparent, members can trust that their savings and loans are being managed responsibly. This begins with leaders who communicate clearly and consistently by explaining how loans are approved, how savings are handled, and how policies evolve as the SACCO grows. Members should feel informed rather than left guessing, and communication should be regular enough that no one is surprised by changes in fees, interest rates, or lending rules.

Equally important is the quality of record‑keeping. A well‑run SACCO maintains accurate books, keeps proper documentation of member transactions, and subjects its accounts to independent audits. These practices protect members from mismanagement and help the SACCO demonstrate credibility to regulators, banks, and potential partners. When records are sloppy or inaccessible, it becomes difficult for members to understand the true financial position of their cooperative and easy for errors or misuse to go unnoticed.

Strong SACCOs also create space for members to participate meaningfully in decision making. Beyond attending annual meetings, it means having a voice in how the SACCO is run, how profits are shared, and how leaders are chosen. Participation reinforces the cooperative spirit and ensures that leadership remains accountable to the people it serves. When members are engaged, they are more likely to monitor performance, question irregularities, and contribute ideas that strengthen the institution.

Accountability is the final pillar. Effective SACCOs establish mechanisms that ensure leaders answer for their decisions, whether through regular reporting, oversight committees, or clear disciplinary procedures. Accountability protects the SACCO from becoming overly dependent on a single individual and reduces the risk of fraud or mismanagement. It also reassures members that leadership is not operating in secrecy or without checks and balances.

In essence, governance is where the promise of a SACCO is either fulfilled or undermined.

Conclusion

SACCOs have become one of the most meaningful expressions of financial inclusion in Uganda because they demonstrate that trust, proximity, and shared purpose can function as real economic infrastructure. They show that people do not need complex financial products to participate in formal finance; they need institutions that recognise their realities and give them a stake in how their money is managed. Their continued relevance will depend on how well they evolve without losing this foundation.

Strong governance, transparent leadership, and regulatory discipline are the conditions that allow SACCOs to grow responsibly as deposits rise and member needs diversify.