Upfront Costs and Why Banks Charge Them

Upfront costs are the fees and charges you must pay when taking out a loan, before or at disbursement. They include items such as application fees, loan arrangement (origination) fees, processing fees, CRB checks, valuation and legal fees, and mortgage registration. Banks make these charges for the following main reasons:

- To recover processing and setup costs. Origination or arrangement fees cover the lender’s cost of evaluating your application, performing credit checks, and setting up the loan account. These fees are a one time charge that helps banks cover administrative expenses.

- To compensate for risk and capital commitment. Commitment or arrangement fees can reflect the cost of reserving funds for you and the credit risk the lender assumes while your loan is being processed.

- To pay third party service providers. Valuation, registration, legal, and some insurance fees are often paid to external parties (valuers, land registries, law firms, insurers) rather than the bank; the lender passes these costs to the borrower.

- To cover ongoing account administration. Processing and service fees help maintain loan accounts, manage repayments, and provide customer support over the life of the loan.

Why You Need to Know Your Upfront Loan Costs

- They affect how much you actually receive. For example, if you borrow UGX 60 million but pay UGX 1.5 million in upfront fees, you effectively receive less money than you expected. This can disrupt your plans, especially for business loans, school fees, or construction projects.

- They vary widely across banks. Different banks charge different fees. Some banks list fixed amounts, others list percentages. It is important to understand how these fees are computed by your chosen lender.

- They influence your true cost of borrowing. Interest rates alone don’t tell the full story. Upfront fees increase your effective loan cost, such that a loan with a lower interest rate but high upfront fees may be more expensive overall.

- The power to negotiate. When you know what other banks charge, you can negotiate better. Some fees like application fees or processing fees are sometimes discounted for strong clients.

- Protect yourself from surprises. Many borrowers only learn about valuation fees, legal fees, or insurance charges at the final stage. Understanding these costs early helps you plan your cash flow and avoid delays in loan approval.

A practical caution

Requests to pay fees before any funds are disbursed can be a red flag for fraud; legitimate lenders typically deduct fees from the loan proceeds or itemise them in the loan agreement rather than demanding advance payments to unknown accounts. Always confirm fee collection methods with the lender.

Introducing the Simply Mint Upfront Loan Cost Calculator

Simply Mint’s Upfront Loan Cost Calculator is a quick, user‑friendly tool that estimates the minimum cash you must pay before a loan is released.

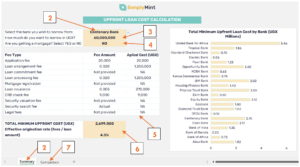

The calculator brings together the key elements of a loan assessment in one place. It begins with a section where you choose your bank, enter your loan amount and indicate whether the loan is a mortgage, which allows the tool to tailor the fees that apply. It then presents a detailed breakdown of all the upfront charges associated with that selection alongside the applied cost in shillings. The final section summarises your total minimum upfront cost and effective origination rate and includes a comparison view that displays the same structure across multiple lenders so you can see how different banks stack up and make a more informed borrowing decision.

Definitions of the Types of Fees Included in the Calculator

- Application fee: A charge for submitting your loan application.

- Loan arrangement fee: Fee for structuring the loan; often a percentage of the principal.

- Loan commitment fee: Charge for reserving funds for you prior to disbursement.

- Loan processing fee: Administrative cost for evaluating and approving the loan.

- Mortgage registration: The cost to register the mortgage at the land registry; often depends on property value.

- Loan insurance: Insurance premium that protects the lender and sometimes the borrower.

- Credit reference bureau check fee: Fee for checking your credit history with a credit reference bureau.

- Security valuation fee: Payment to a valuer to assess your pledged asset; often charged by a third party.

- Security search fee: Cost of searching land records to confirm ownership and encumbrances.

- Legal fees: Charges for preparing loan and mortgage documents; usually set by law firms or third parties.

How to Use the Simply Mint Upfront Loan Cost Calculator

- Download the calculator through this link: SimplyMint_Loan_Upfront_Cost_Calculator

- In the Summary tab, select your bank. Choose the lender from the dropdown list.

- Enter the loan amount in UGX. Type the number without commas (for example 60000000 for UGX 60,000,000).

- Indicate whether it is a mortgage by selecting YES or NO. This will return mortgage‑specific fees.

- Review the fee breakdown. The tool lists each Fee Type, the Fee Amount (fixed or percentage), and the Applied Cost (UGX).

- Check totals. The calculator shows TOTAL MINIMUM UPFRONT COST (UGX) and the Effective origination rate (fees / loan amount) so you can see the minimum cash you must have and the fee share of the loan.

- Compare banks. Use the Comparison tab to view the same inputs across multiple lenders and spot the best overall offer.

- Save or print your results. Bring the printed breakdown to the bank and ask them to confirm each fee in writing.

How to Interpret Special Labels

- When a fee is marked “Not Provided”, the bank did not supply that charge in its publicly available tariff guide. You should ask the banks to confirm whether the fee applies to your loan and the exact amount.

- “Actual” means the service fee is charged by a third party or is case dependent. Fees shown as “Actual” often depend on the value of the security, the third‑party service provider (for example, valuers, registries, or law firms), or other case‑by‑case factors. These charges are typically set outside the bank’s fixed tariff. Ask your bank for an itemised estimate and, where possible, written confirmation of who will charge the fee and how it will be calculated.

- Minimum vs final cost. The tool computes the minimum cost based on publicly available tariff items. Final costs may include additional ancillary charges, taxes, or third‑party fees not captured in the public tariff. Always request a full, written fee schedule from the lender before signing.

Important Disclaimer

The calculator is a decision‑support tool that computes the minimum upfront cost you should expect to pay for a personal loan in UGX based on information publicly availed by the financial service provider (FSP). It does not list every possible charge. Borrowers must confirm the full set of charges with their FSP before accepting any loan. Fees are likely to be higher than the calculator’s minimum estimate once ancillary or case‑specific charges are included.

While You’re Here…

Check out our table of all loan-related charges to compare across banks.